Crisis, what crisis?

I picked this up on Bloomberg, not an obvious conspiracy theory merchant.

Have a look at this chart:

What it shows is the movement of LIBOR compared with the CDS for the banks that make up the LIBOR panel. Explanation needed! LIBOR is the rate at which major London banks lend money to each other. It is calculated by the banks based on their estimate of what they would have to pay if they borrowed money from each other. The chart shows that the Cyprus crisis has not caused a ripple in the LIBOR rate.

At the same time the Credit Default Swaps (CDS) soared as the Cyprus crisis developed. CDS represents the insurance premium that a bank has to pay to cover any loan it makes to another bank overnight. They have risen by up to 15%. The LIBOR rate has increased by a mere 1.4%. The discrepancy suggests that the banks are continuing to underestimate the interest costs that they might incur in the interbank market.

They can underestimate because, at present, banks do not need to borrow from each. They have other sources of finance (QE?) So they have to guess at the rate. The chart suggests that they are continuing to underestimate. You will recall that several banks were fined because of cheating by underestimating the LIBOR rate at the time of the 2008 banking crisis.

What is the incentive for banks to cheat? If they show that they would incur low rates of interest if they run out of cash and need to borrow, it gives the impression that they are less at risk of financial stress. The rise in CDS shows that the companies offering insurance against a bank default believe that the risk of default is rising significantly.

I regard the Cyprus banking crisis and the system adopted for solving it as a major break with the past. We can no longer view people who want to stash their money under a mattress as oddballs. There is a real risk that customers will withdraw their funds from weaker banks right across Europe. Lower LIBOR rates can help to mask weakness.

Does this have an implication for stock prices? It certainly does. If interest rates are perceived to be low, and LIBOR is an important contributor to the measure of interest rates, then stocks will be viewed as offering a better return on money. If interest rates are seen as rising, the attraction of stocks diminishes and prices will fall.

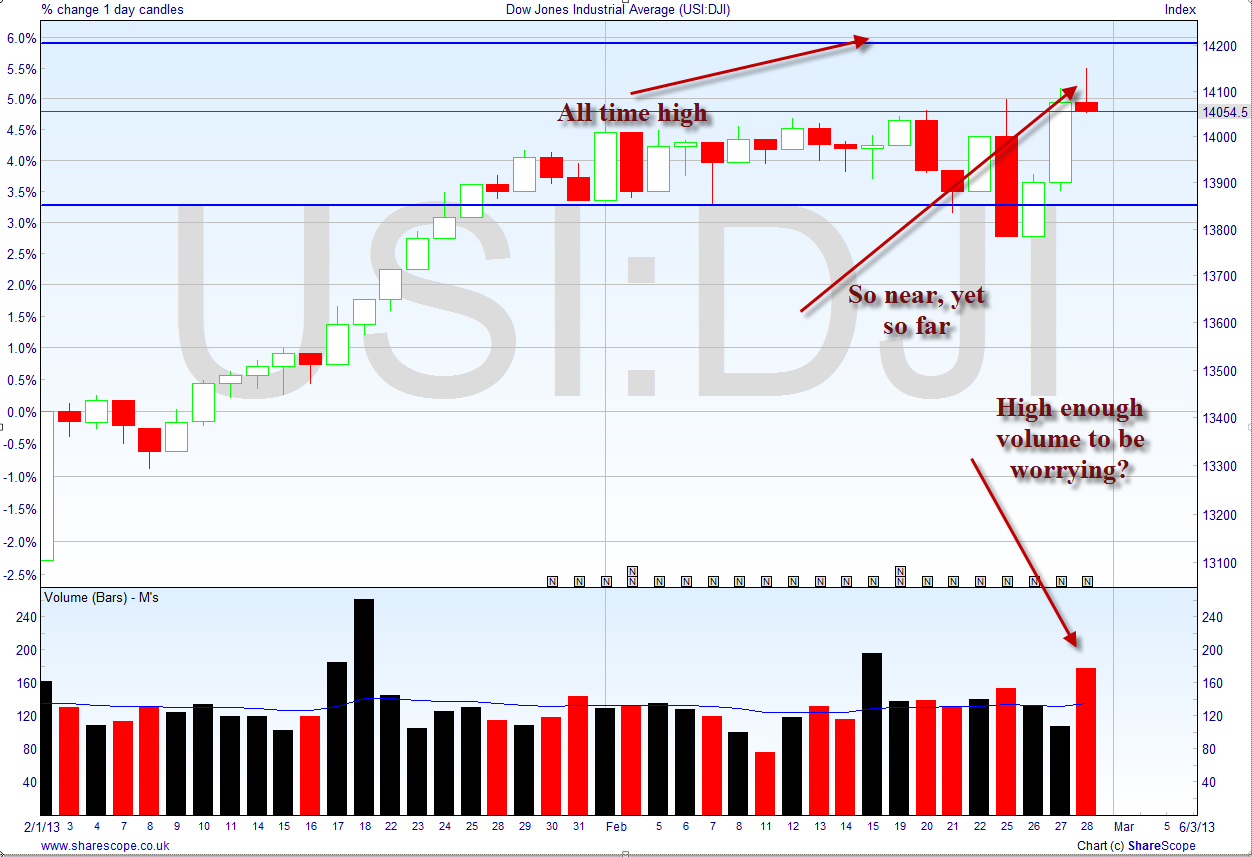

What the markets think

In the meantime, back in the real world, the Dow is having a go at breaking out of its channel. Not enough to tempt me. If we get no more than this I shall just widen the channel and see what happens next.

It is one of those classic struggles between the bulls and the bears. The bulls are buying, pushing prices higher while the bears take advantage of these high prices to offload more of their portfolios. At this stage, under normal circumstances, news would drive the market. But seeing how the biggest assault on ordinary bank depositors has been ignored by the market, something quite different is going on.

Old Blog

I used to write a blog about the way that I saw the world. I stopped about three years ago. I am amazed that it still attracts 15 - 20 readers per day directed there by Google. Most of my hits these days are to an article I wrote about the Sunni Shia conflict, one about the terrible things that the Australian Government did to children in the 1950s and another about political corruption. A popular topic was my description of the sub prime mortgage crisis, though interest there is, understandably, fading.

I was very surprised that there were two hits, in quick succession to a post that I called Damart Days. It is a little essay on getting older. I would have forgotten about it altogether if it was not for these unexpected visitors. If you would like to have a look click here.